You Served. You Earned This — The Truth About VA Home Loans

November 11, 2025

November 11, 2025

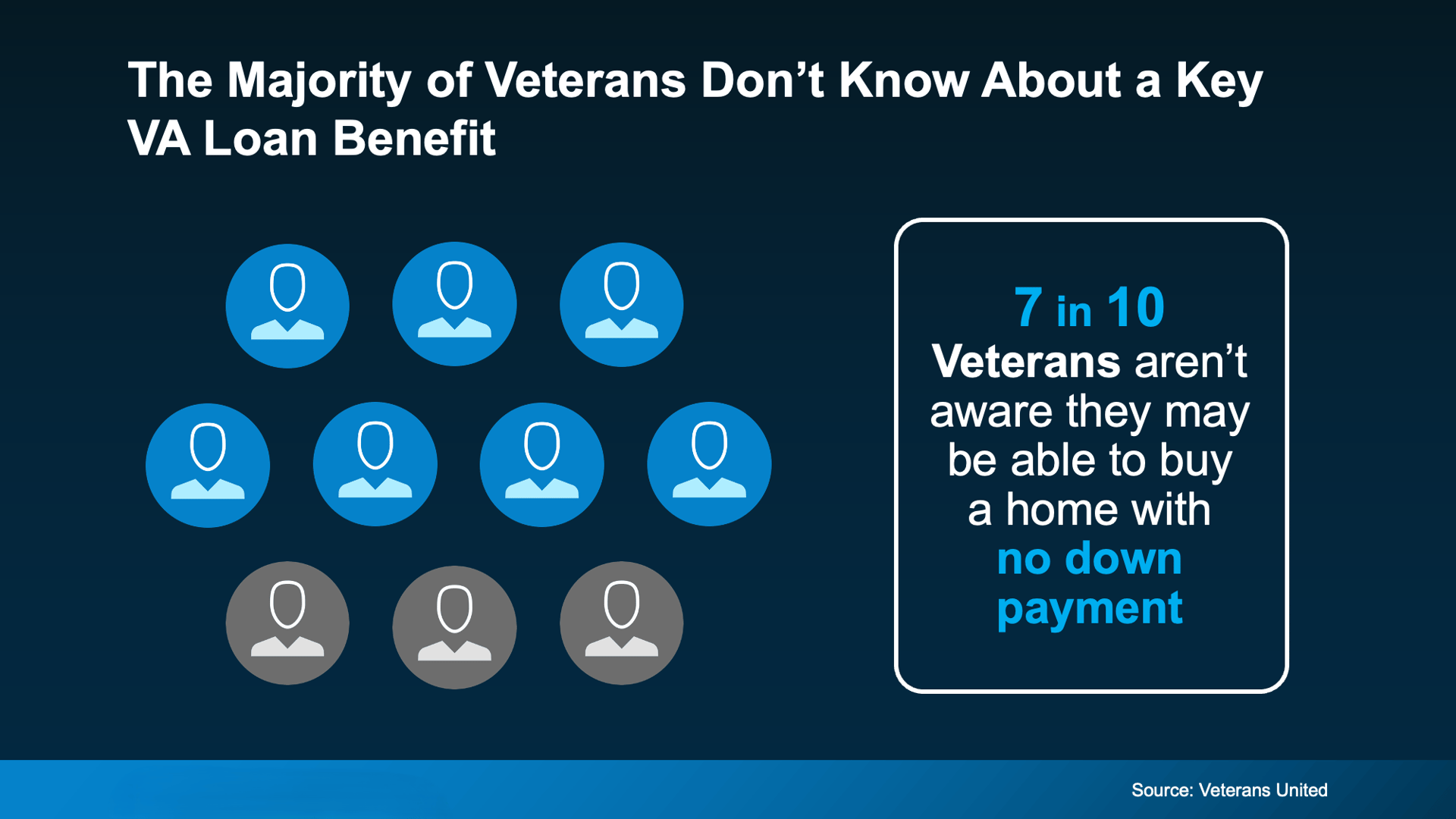

Most Veterans Don’t Know They Can Buy a Home with $0 Down

If you’ve served in the military—or your spouse has—you’ve earned one of the most powerful homebuying tools out there: the ability to buy a home with no down payment.

But here’s the surprising part: 70% of Veterans don’t know about it.

That’s according to Veterans United, and it means 7 out of 10 Veterans are missing out on one of their biggest earned benefits. Let’s change that.

For nearly 80 years, VA loans have made homeownership possible for millions of Veterans and active-duty service members. Here’s why they’re still one of the best loan options out there, straight from the Department of Veterans Affairs:

✅ $0 Down Payment: Skip years of saving and get into a home sooner.

✅ Lower Upfront Costs: The VA limits which closing costs Veterans have to pay, so you keep more cash at closing.

✅ No Private Mortgage Insurance (PMI): That means lower monthly payments compared to many other loan types.

Bottom line: VA loans are designed to make homeownership more achievable for those who’ve served—and to keep costs down while doing it.

Lately, there’s been confusion about whether VA loans are still available during a government shutdown. The short answer: yes, they are.

According to Veterans United:

“The good news is that the shutdown has minimal impacts on VA lending. Lenders are still able to order appraisals, obtain a borrower’s Certificate of Eligibility, submit the VA Funding Fee and more. In short, Veterans are still able to use their home loan benefit to buy a home or refinance an existing mortgage.”

So while you may see minor processing delays, the VA loan program is still running. You can apply, qualify, and close on your new home—just be prepared for a little extra patience.

Navigating a VA loan is easier when you’ve got the right people in your corner. VA News puts it best:

“Choosing a military-friendly broker or agent who understands the VA home loan application process can make all the difference in the homebuying experience.”

Here’s what that looks like in practice:

Your agent helps you find homes that qualify for VA financing.

Your lender helps you get the paperwork, appraisal, and funding squared away.

Both work together to keep your deal on track, even if delays pop up.

Communication is key—and so is experience with VA transactions.

If you’ve served, you’ve earned the right to buy a home with one of the best loan programs available. VA loans offer:

No down payment

Lower upfront costs

No PMI

Flexible qualification standards

And yes—even during a government shutdown—they’re still available.

If you’re ready to explore your options, talk to a VA-approved lender or a local military-friendly agent who can walk you through every step.

Because when it comes to homeownership, you’ve already done the hard work—you deserve to enjoy the benefits.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

[email protected]

1345 Park St. Paso Robles, CA 93446

DRE# 01925434

Amber Johnson | March 12, 2026

Amber Johnson | March 12, 2026

Looking for a 3 bedroom rental in Paso Robles? This well-maintained townhome located at 861 Marlbank Place offers comfortable living, a 2-car garage, stainless steel a… Read more

Amber Johnson | March 10, 2026

Amber Johnson | March 10, 2026

Amber Johnson | March 7, 2026

Amber Johnson | March 6, 2026

Amber Johnson | March 6, 2026

Amber Johnson | March 5, 2026

Amber Johnson | March 5, 2026

You’ve got questions and we can’t wait to answer them.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

DRE# 01925434

1345 Park Street

Paso Robles, CA 93446