Why Waiting for 5.99% Might Cost You More Than You Think

October 29, 2025

October 29, 2025

Why Waiting for 5.99% Might Cost You More Than You Think

Mortgage rates have been the monster under the bed for a while. Every time they tick up, people flinch and say, “Maybe I’ll wait.”

But here’s the twist — waiting for that perfect 5-point-something rate could end up haunting your wallet later.

According to the National Association of Realtors (NAR):

“. . . a 30-year fixed rate mortgage of 6% would make the median-priced home affordable for about 5.5 million more households—including 1.6 million renters. If rates were to hit that magic number, it’s likely that about 10%—or 550,000—of those additional households would buy a home over the next 12 or 18 months.”

That “magic number” — 6% — is what so many buyers are waiting for.

And as expert forecasts suggest, we may see that happen in 2026. But here’s the catch: once that shift happens, it’s going to wake the market back up.

When rates drop into that psychological sweet spot, more buyers will jump in — and that surge in demand will drive home prices higher.

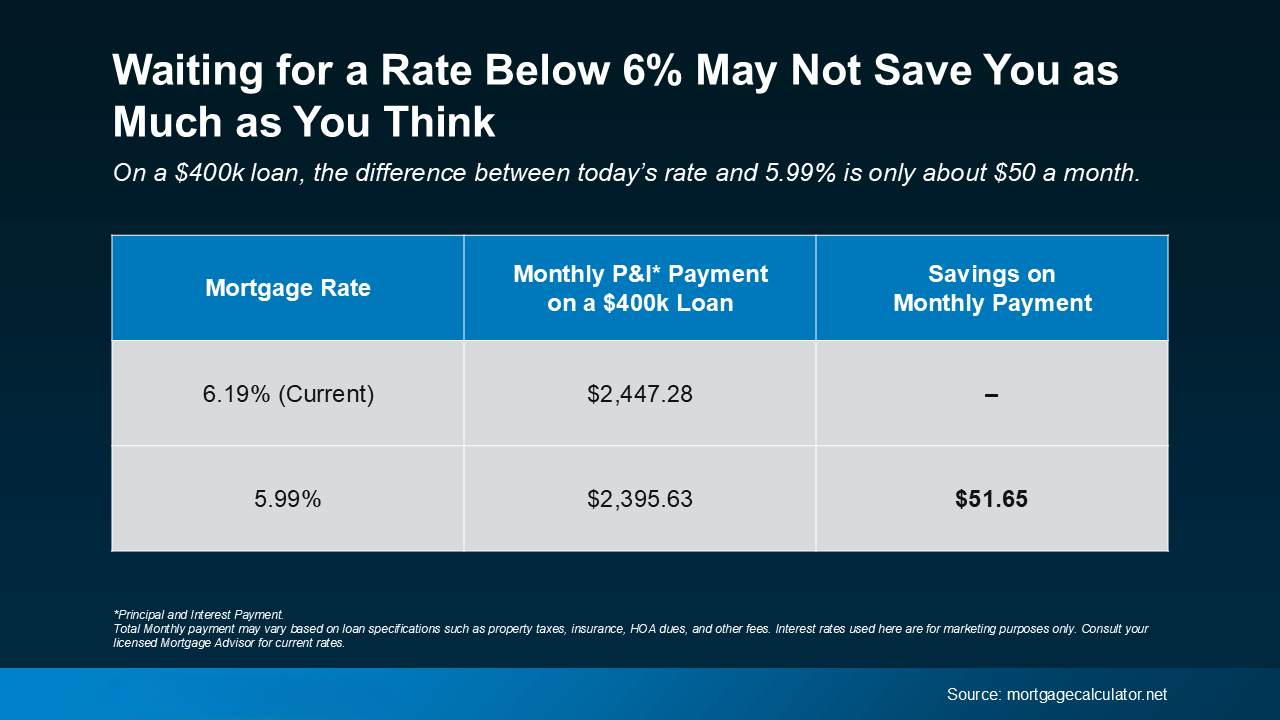

Let’s put some numbers to it.

On a $400,000 mortgage, the difference between today’s rate (around 6.2%) and that coveted 5.99% is roughly $50 a month.

That’s less than a couple of coffee runs or a few takeout orders each month.

But if home prices rise when more buyers rush in, you could easily lose that savings — and then some.

So, while it’s tempting to wait for that lower rate, the math shows it might not actually help you as much as you think.

Right now, you’ve got the advantage of:

✅ More homes to choose from

✅ Better negotiating power

✅ Less competition from other buyers

Once rates dip below 6%, those benefits start disappearing fast.

Jessica Lautz, Deputy Chief Economist and VP of Research at NAR, explains:

“Over the last 5 weeks, mortgage rates have averaged 6.31%. This has provided savvy buyers a sweet spot to reexamine the home search process with more inventory, widening their choices.”

And Matt Vernon, Head of Retail Lending at Bank of America, adds:

“Rather than waiting it out for a rate that they like better, hopeful homebuyers should assess their personal financial situation—if the house is right for them, and the upfront and monthly payments are affordable, it could be the right chance to make a move.”

In other words — don’t wait for “perfect.” Because when everyone else thinks it’s the perfect time to buy, you’ll be competing with all of them.

If moving at today’s rate still feels scary, remember: waiting doesn’t always pay off.

Once rates dip below 6%, demand (and prices) will climb again.

So instead of chasing the “magic number,” focus on what you can control — your budget, your goals, and your timing.

Because if you’re ready, this might just be your moment to make a move before the market wakes up again.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

[email protected]

1345 Park St. Paso Robles, CA 93446

DRE# 01925434

Amber Johnson | February 28, 2026

Amber Johnson | February 27, 2026

Amber Johnson | February 27, 2026

Amber Johnson | February 27, 2026

Amber Johnson | February 26, 2026

Amber Johnson | February 26, 2026

Amber Johnson | February 26, 2026

Amber Johnson | February 25, 2026

Amber Johnson | February 24, 2026

You’ve got questions and we can’t wait to answer them.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

DRE# 01925434

1345 Park Street

Paso Robles, CA 93446