Is Renting Really Cheaper? Here’s What the Data Says

February 25, 2026

February 25, 2026

Renting can feel like the simpler choice.

No large down payment.

No surprise repair bills.

No long-term commitment.

But then your rent increases. And then it increases again. And suddenly the flexibility starts looking… expensive.

Especially when you realize none of that monthly payment builds equity. And that’s when the cycle starts to feel frustrating.

There’s a lot of noise right now about how buying isn’t affordable. But when you actually look at the numbers, the math may work better than you expect.

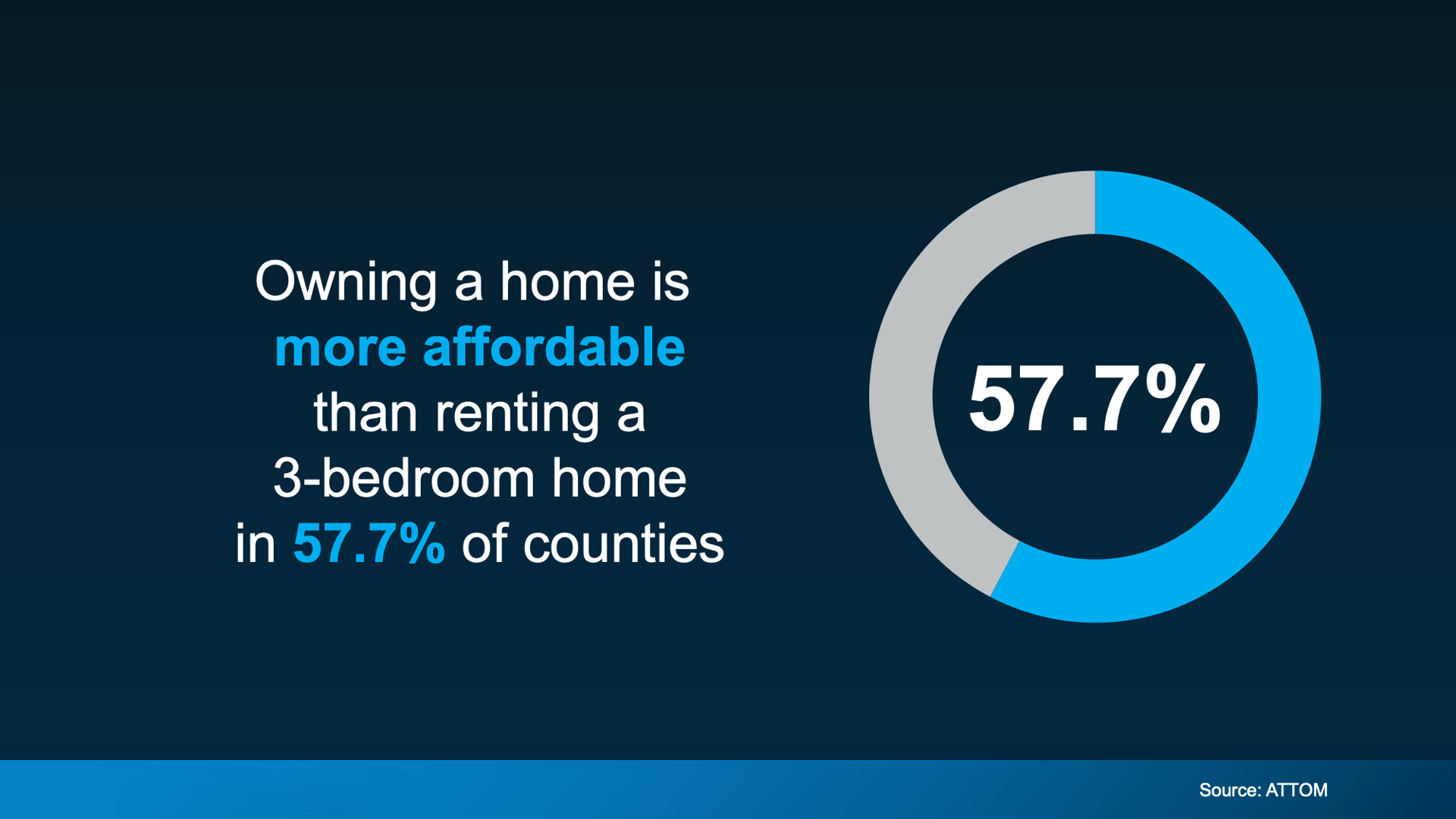

In a surprising number of markets, owning a home is now cheaper on a monthly basis than renting a three-bedroom property.

According to recent data from ATTOM, buying is more affordable than renting in nearly 58% of U.S. counties even after factoring in insurance and typical maintenance costs.

That shift is happening because:

Home price growth has slowed

More homes are available

Mortgage rates have eased compared to last year

While it may not feel obvious, in many areas, rent is stretching budgets more than a mortgage would.

And unlike rent, a mortgage payment builds equity over time.

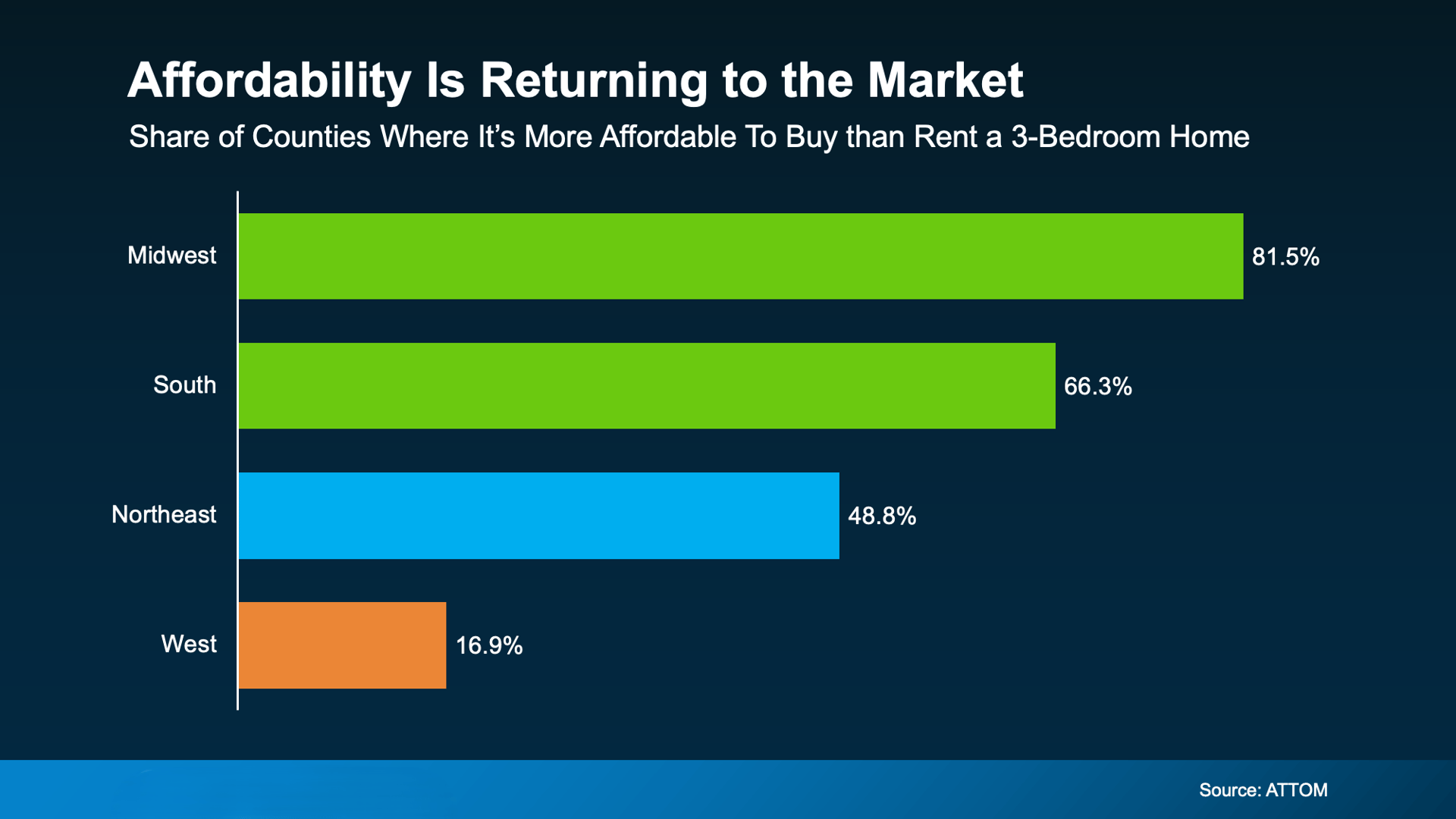

Now, let’s be clear. Buying isn’t cheaper everywhere.

Affordability varies by region. The biggest improvements are happening in parts of the Midwest and South. Some Western markets are still tighter.

That’s why national headlines don’t tell the whole story. The only numbers that matter are the ones in your local market.

Because what feels out of reach in one city may be completely realistic in another.

If you’re thinking, “Okay, but I still don’t have a down payment,” you’re not alone.

For many renters, the biggest obstacle isn’t the monthly payment. It’s the upfront cash required to get started.

Here’s what most people don’t realize: there are thousands of down payment assistance programs available across the country.

And the average benefit? About $18,000.

That can help cover part of your down payment or closing costs, which means you may not need to save as much as you think.

When you combine:

Monthly payments that may be comparable (or lower) than rent

Slower price growth

Easing mortgage rates

And available financial assistance

Buying can shift from “someday” to “maybe sooner than I thought.”

Rent feels flexible. But rising rent increases your housing cost every year without building ownership.

With a fixed-rate mortgage, your principal and interest payment stays stable. And every payment builds equity.

That difference adds up over time.

This isn’t about rushing into a purchase. It’s about running the numbers instead of assuming buying isn’t possible.

Renting isn’t automatically the more affordable option.

In many markets today, buying may cost less monthly than renting, and it builds long-term equity instead of funding someone else’s.

If you’re renting and wondering whether homeownership could work for you, a quick conversation with a local real estate agent or lender can give you clarity.

You don’t need to commit.

You just need real numbers.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

[email protected]

1345 Park St. Paso Robles, CA 93446

DRE# 01925434

Amber Johnson | April 21, 2026

Amber Johnson | April 21, 2026

Amber Johnson | April 21, 2026

Amber Johnson | April 21, 2026

Amber Johnson | April 21, 2026

Amber Johnson | April 20, 2026

Amber Johnson | April 20, 2026

Amber Johnson | April 20, 2026

Amber Johnson | April 20, 2026

You’ve got questions and we can’t wait to answer them.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

DRE# 01925434

1345 Park Street

Paso Robles, CA 93446