Life Changes Are Beating Low Rates: What’s Really Driving Sellers Today

December 5, 2025

December 5, 2025

If you’re like a lot of homeowners, you’ve probably had this thought:

“I want to move… but I don’t want to give up my 3% rate.”

Totally fair. That rate has been one of your best financial wins. But here’s the part people forget:

A great rate can’t fix a home that no longer fits your life.

And life eventually wins.

You’re not the only one feeling stuck — and you’re not the only one finally deciding to move anyway.

For years, homeowners stayed frozen in place, locked into their old ultra-low rates. But that grip is loosening.

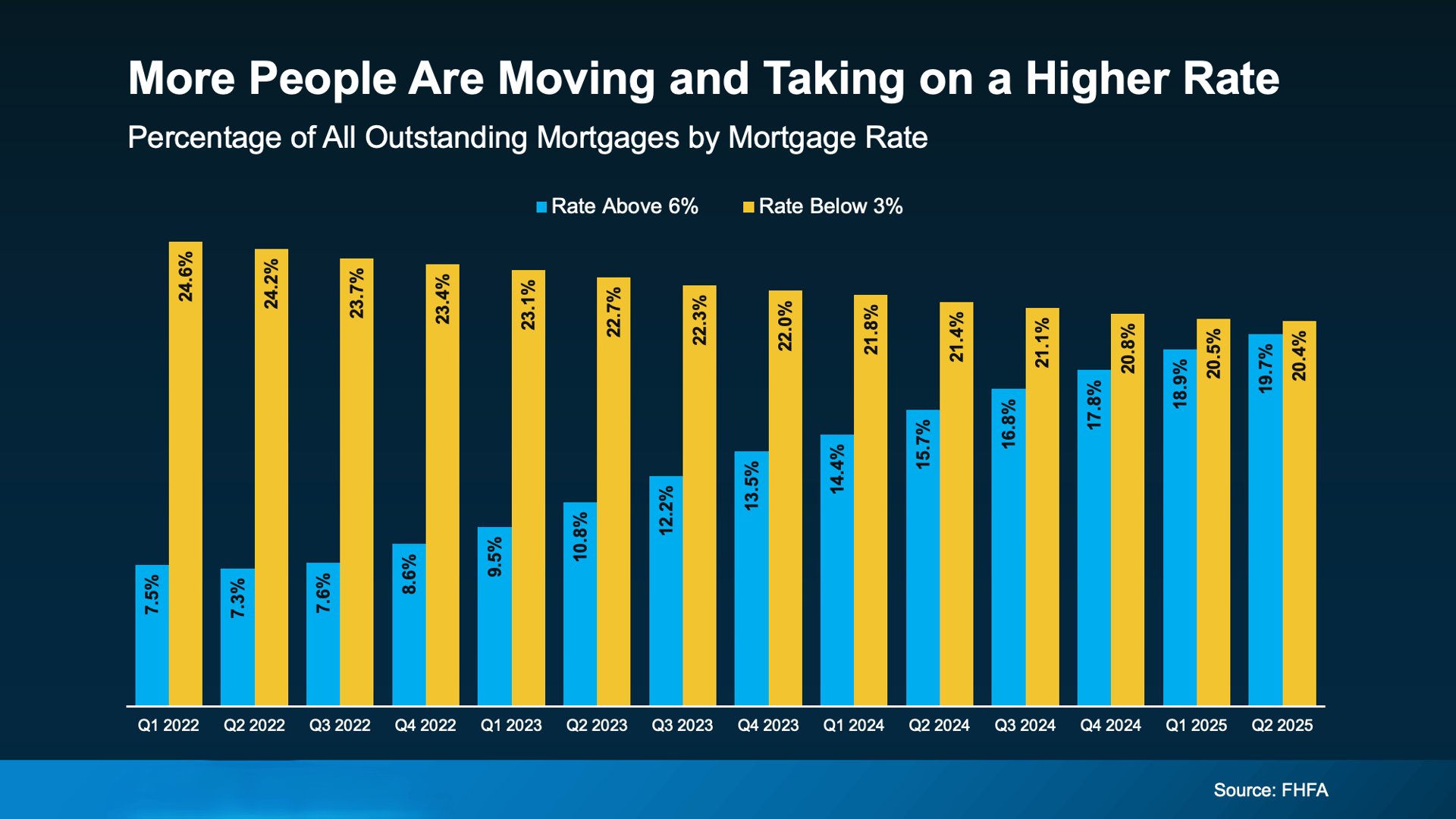

Data from the FHFA shows:

The share of homeowners with rates below 3% is slowly shrinking

The share of homeowners with rates above 6% is rising

Yes — people are taking on today’s rates to move forward.

And here’s the wild part:

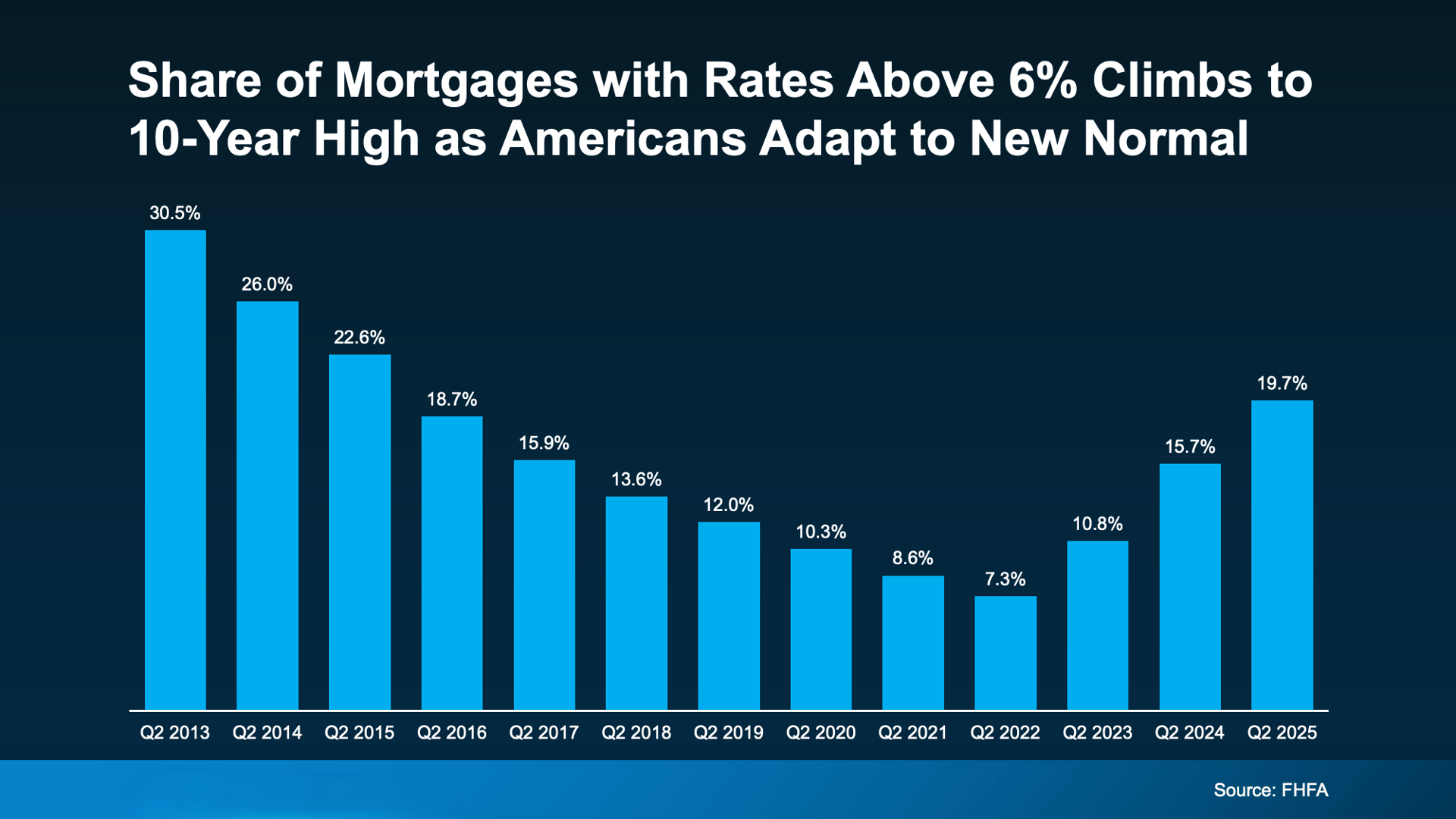

Mortgages with rates above 6% just hit a 10-year high.

That’s proof the mindset is shifting. More people are accepting today’s rates as “normal” so they can actually live their lives.

Easy. Because real life doesn’t care about mortgage rates.

As Redfin’s Chen Zhao puts it:

“Life doesn’t stand still… needs are starting to outweigh the financial benefit of clinging to a rock-bottom mortgage rate.”

Translation: life is happening whether we like it or not.

First American calls them the 5 Ds — the real reasons people move:

You’re earning more, your career has grown, and the starter home you bought years ago just isn’t cutting it.

A new baby means your house just shrank by about 1,000 square feet overnight.

Ending or beginning a relationship often means finding a home that works for your new life.

The kids are out. The extra rooms are empty. You’re paying to heat, cool, and clean space you don’t use.

Losing someone often shifts your priorities fast. Being closer to family matters more than your interest rate.

These are the things that actually drive moves — not rates.

Realtor.com says almost 2 in 3 potential sellers have been thinking about moving for more than a year.

That’s a long time to press pause on your life.

So maybe the real question isn’t:

“Should I move?”

It’s:

“How long am I willing to stay in a house that no longer fits my life?”

Rates hit 7%+ earlier this year. They’ve since eased into the low 6s — and experts expect another small dip in 2026.

No crash. No miracle. Just slow, steady improvement.

Combine that with a life change you can’t ignore… and suddenly the move you’ve been putting off might make sense.

Life doesn’t wait for a perfect rate — and neither should you.

Rates are down from their peak. They’re expected to ease a bit more. And you only get one life, not one interest rate.

If you’re thinking about making a move, talk with a local agent and lender. You might be surprised by what’s possible right now.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

[email protected]

1345 Park St. Paso Robles, CA 93446

DRE# 01925434

Amber Johnson | July 27, 2026

Amber Johnson | July 27, 2026

Amber Johnson | July 27, 2026

Amber Johnson | July 27, 2026

Amber Johnson | July 27, 2026

Amber Johnson | July 27, 2026

Amber Johnson | July 23, 2026

Amber Johnson | July 23, 2026

Amber Johnson | July 23, 2026

You’ve got questions and we can’t wait to answer them.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

DRE# 01925434

1345 Park Street

Paso Robles, CA 93446