Why Fed Rate Cuts Don’t Always Mean Cheaper Mortgages

September 15, 2025

September 15, 2025

The Federal Reserve (the Fed) meets this week, and expectations are high that they’ll cut the Federal Funds Rate. But does that mean mortgage rates will drop? Let’s clear up the confusion.

Right now, all eyes are on the Fed. Most economists expect they’ll cut the Federal Funds Rate at their mid-September meeting to help fend off a potential recession.

But here’s what you need to know: the Fed doesn’t actually set mortgage rates. Instead, they set the short-term rate banks charge each other. That ripples through the economy and impacts borrowing costs, but mortgage rates are influenced by a mix of factors like inflation, investor confidence, and economic data.

So while the Fed doesn’t control mortgage rates, their actions can still influence the direction they take.

Here’s where it gets interesting. Mortgage rates often respond before the Fed makes a move. That’s because financial markets tend to price in what they think the Fed is going to do ahead of time.

That’s why rates dipped after the weaker-than-expected jobs reports on August 1 and September 5. Investors grew more confident a cut was coming, and mortgage rates adjusted accordingly.

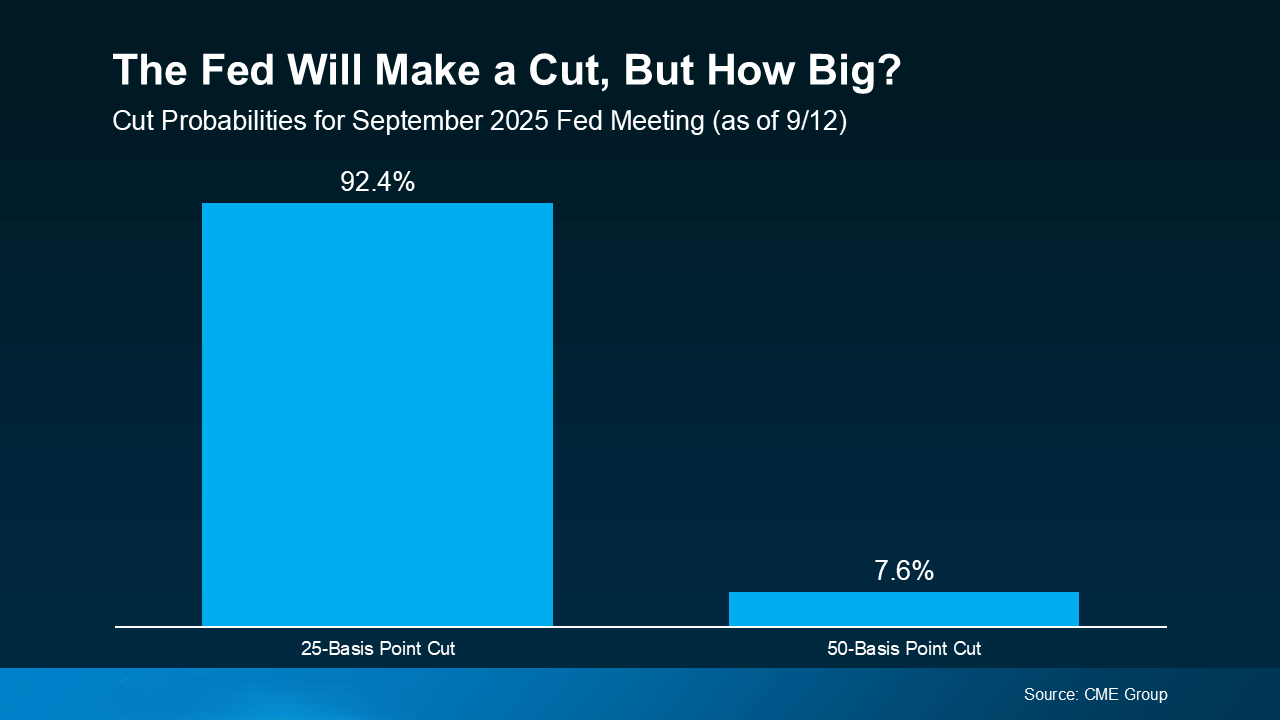

So, if the Fed goes with the expected 25-basis point cut, chances are mortgage rates won’t move much — because it’s already “baked in.” But if the Fed surprises markets with a bigger 50-basis point cut, rates could fall more noticeably.

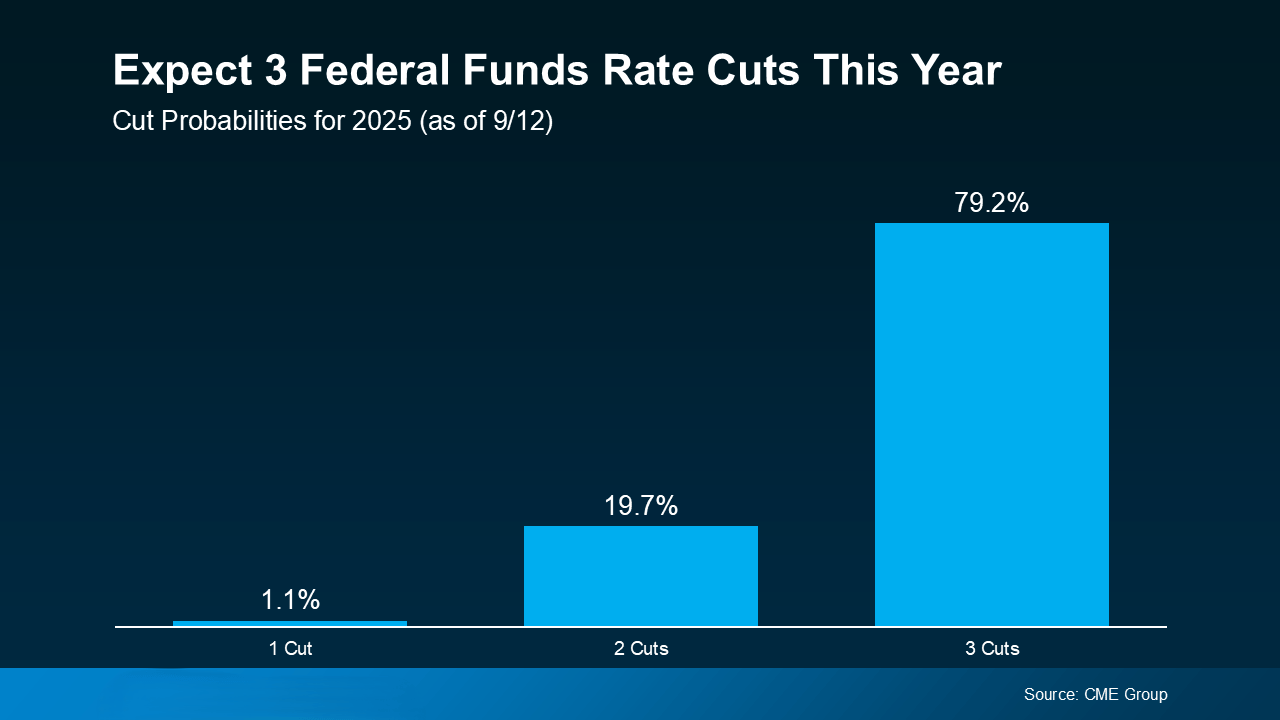

Even if this week’s cut doesn’t lead to a huge change, experts say more could be on the horizon. Many economists expect the Fed to cut rates again before the end of the year if the economy continues to slow.

And that could matter for you. As Sam Williamson, Senior Economist at First American, explains:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

In other words: if multiple cuts happen, or even if markets just believe they will, mortgage rates could trend lower into 2026.

But remember — this all depends on how the economy unfolds. Inflation surprises, unexpected job growth, or policy shifts could all change the path forward.

Mortgage rates won’t move lockstep with the Fed, but a cycle of rate cuts could bring some relief over time.

If you’ve been waiting for better affordability, it’s worth keeping a close eye on what happens next. Even a small dip in rates can mean real monthly savings — and the right opportunity for you to make your move.

Talk with your agent and lender to run the numbers so you’re ready when the market shifts.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

[email protected]

1345 Park St. Paso Robles, CA 93446

DRE# 01925434

Amber Johnson | May 29, 2026

Amber Johnson | May 29, 2026

Amber Johnson | May 29, 2026

Amber Johnson | May 29, 2026

Amber Johnson | May 29, 2026

Amber Johnson | May 28, 2026

Amber Johnson | May 28, 2026

Amber Johnson | May 28, 2026

Amber Johnson | May 28, 2026

You’ve got questions and we can’t wait to answer them.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

DRE# 01925434

1345 Park Street

Paso Robles, CA 93446