Facing Hardship? What Today’s Foreclosure Trends Really Mean

September 3, 2025

September 3, 2025

You may be seeing headlines about how foreclosures are rising. And if that makes you nervous that we’re headed for another crash, here’s what you should know.

According to ATTOM, during the housing crash, over nine million people went through some sort of distressed sale (2007–2011). Last year? Just over 300,000.

So, even with the recent uptick, we’re talking about numbers that are dramatically lower. But what about the future? Is another wave coming? The short answer: no.

Experts watch mortgage delinquencies (loans more than 30 days past due) as an early signal for potential foreclosures. And the latest data is actually reassuring.

Right now, delinquencies overall are consistent with where we ended last year. That means there’s no sharp increase signaling widespread trouble.

But there’s one nuance worth noting. Marina Walsh, Vice President of Industry Analysis at the Mortgage Bankers Association, explains:

“While overall mortgage delinquencies are relatively flat compared to last year, the composition has changed.”

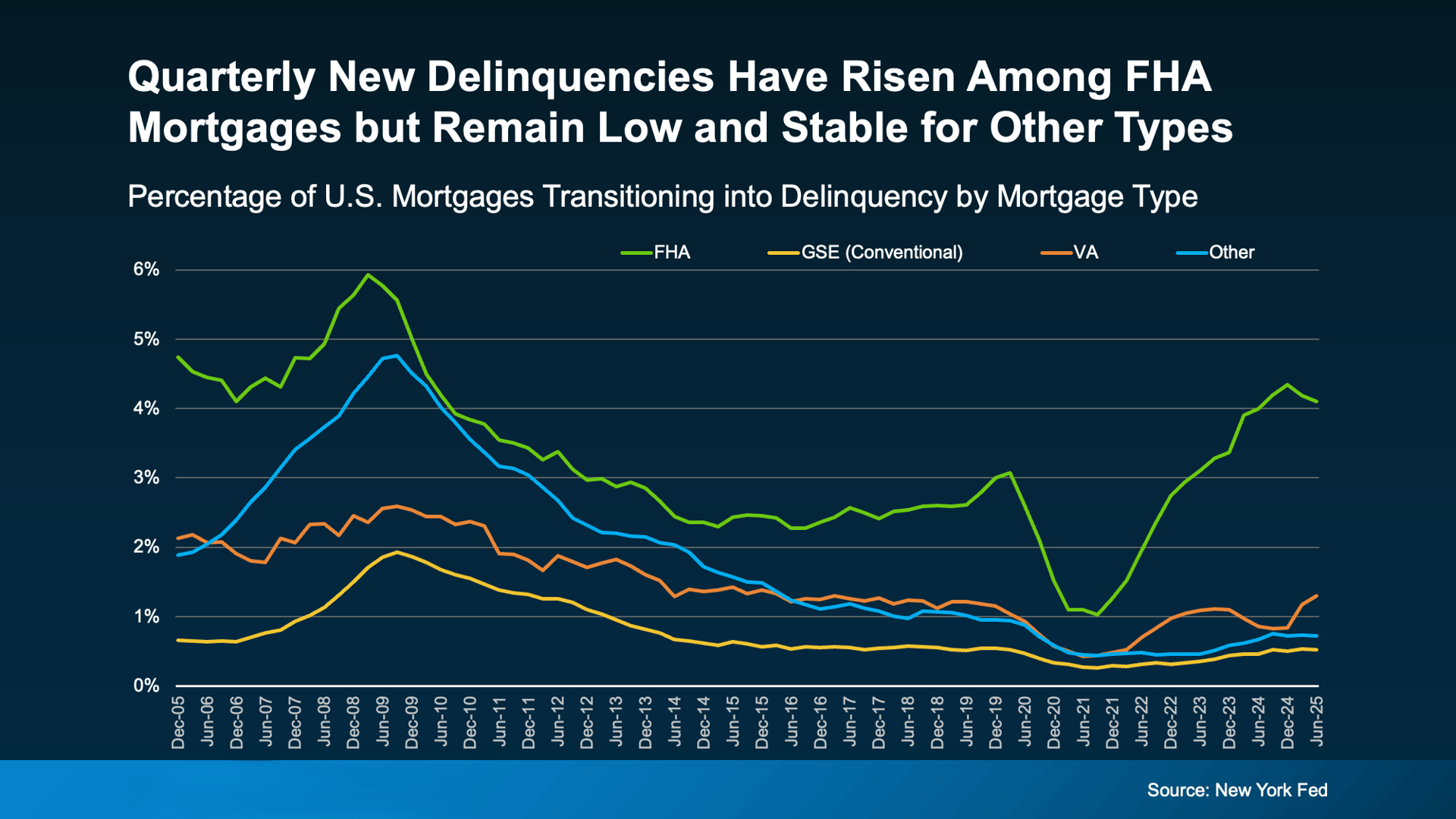

Today, borrowers with FHA mortgages make up the biggest share of new delinquencies (see graph).

Why? Borrowers with FHA loans often have smaller down payments and lower credit scores, which makes them more sensitive to shifts in the economy. With stubborn inflation, recession concerns, and employment challenges, it’s not surprising this group is feeling more strain.

But this does not mean the housing market is in danger. Here’s why:

Delinquency rates for other loan types remain low and stable.

During the 2008 crash, delinquencies spiked across all loan types. That’s not the case today.

FHA loans only make up about 12% of all mortgages nationwide.

As ResiClub explains:

“The recent uptick in mortgage delinquency seems to be concentrated among FHA borrowers, however, mortgage performance remains very solid when viewed in light of the twenty-year history of our data.”

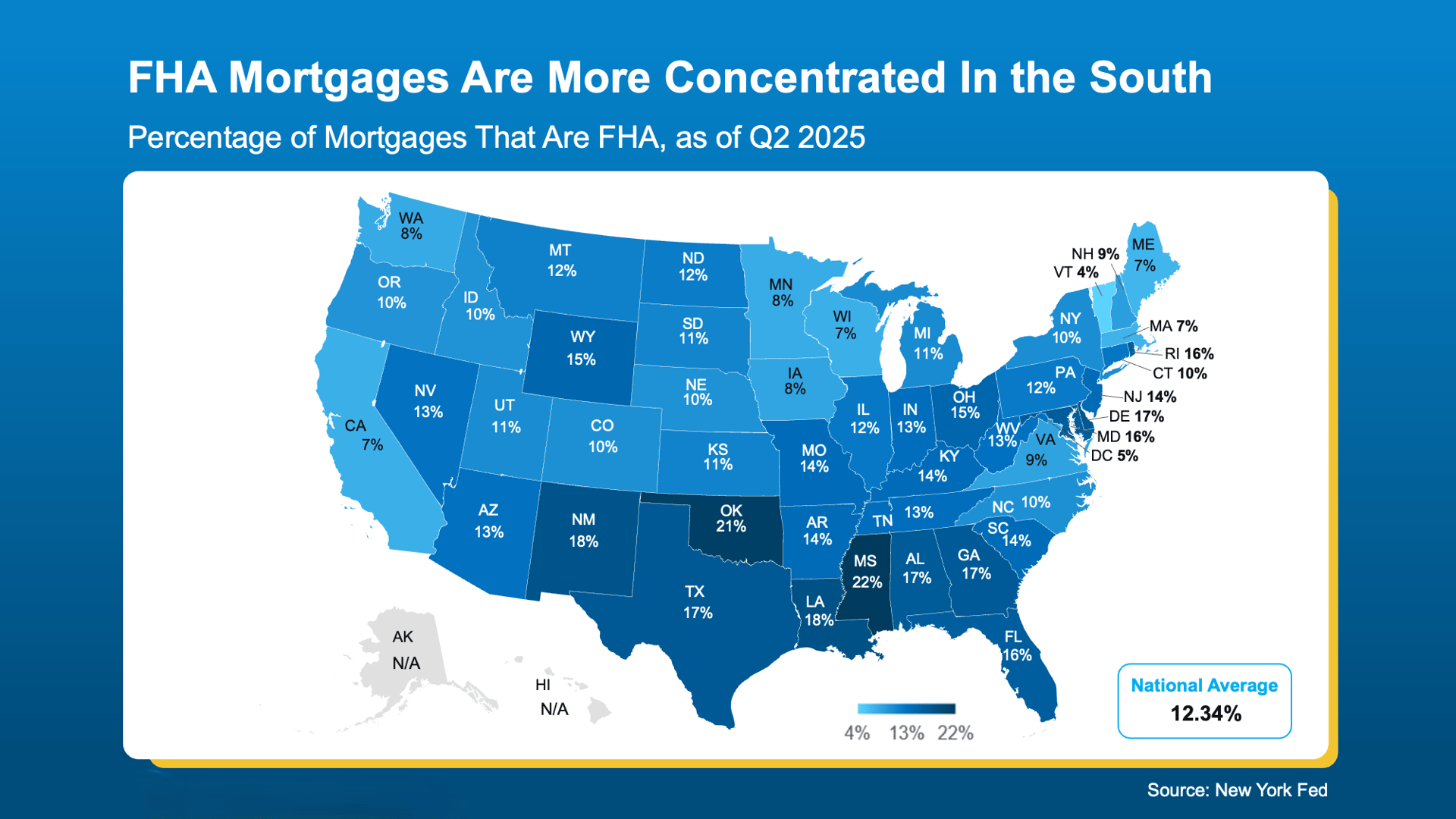

FHA loans are more concentrated in the South. That’s why delinquency numbers are higher in those states compared to the rest of the country.

But even in those areas, today’s delinquency rates are still far lower than 2008 levels. This isn’t a repeat of the past—it’s a sign that certain segments of the market are under more pressure, not that the entire housing system is in trouble.

No one wants to see a homeowner go through foreclosure. If you’re struggling with payments, you’re not alone — and you do have options:

Call your mortgage provider. Many lenders will work with you on repayment plans or loan modifications.

Tap into your equity. With near-record homeowner equity today, many struggling owners may choose to sell instead of foreclosing — and still walk away with money in their pocket.

Foreclosures are up slightly, but they’re nowhere near 2008 levels. The data shows the market is still on strong footing, and delinquency rates don’t point to a crash ahead.

If you want to keep up with the latest shifts in the market, connect with a local real estate agent. They’ll help you separate fact from fear and understand what’s really happening in your area.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

[email protected]

1345 Park St. Paso Robles, CA 93446

DRE# 01925434

Amber Johnson | March 17, 2026

Amber Johnson | March 12, 2026

Amber Johnson | March 12, 2026

Looking for a 3 bedroom rental in Paso Robles? This well-maintained townhome located at 861 Marlbank Place offers comfortable living, a 2-car garage, stainless steel a… Read more

Amber Johnson | March 10, 2026

Amber Johnson | March 10, 2026

Amber Johnson | March 7, 2026

Amber Johnson | March 6, 2026

Amber Johnson | March 6, 2026

Amber Johnson | March 5, 2026

You’ve got questions and we can’t wait to answer them.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

DRE# 01925434

1345 Park Street

Paso Robles, CA 93446