Could an ARM Help You Buy a Home in Today’s Market?

May 22, 2025

May 22, 2025

Adjustable-Rate Mortgages (ARMs): Smart Strategy or Risky Move?

If you’ve been in the market lately, you’ve probably noticed just how much mortgage rates can impact what you can afford. And between today’s rates and rising home prices, many buyers are exploring new ways to make the numbers work.

One option gaining renewed attention? Adjustable-rate mortgages (ARMs).

And if the term “ARM” brings flashbacks to the 2008 housing crash—don’t worry. Things have changed.

ARMs Today Are Not the Same as They Were Then

Back in the mid-2000s, ARMs got a bad reputation because some were offered without proper income checks or realistic payment expectations. Many buyers found themselves in trouble once the rate adjusted and monthly payments jumped.

But that’s not how ARMs work anymore. Today, lenders are much more cautious. They run detailed assessments to make sure you can afford the loan—even after the initial rate period ends and the rate adjusts. In other words, this isn’t about risky lending—it’s about strategic options.

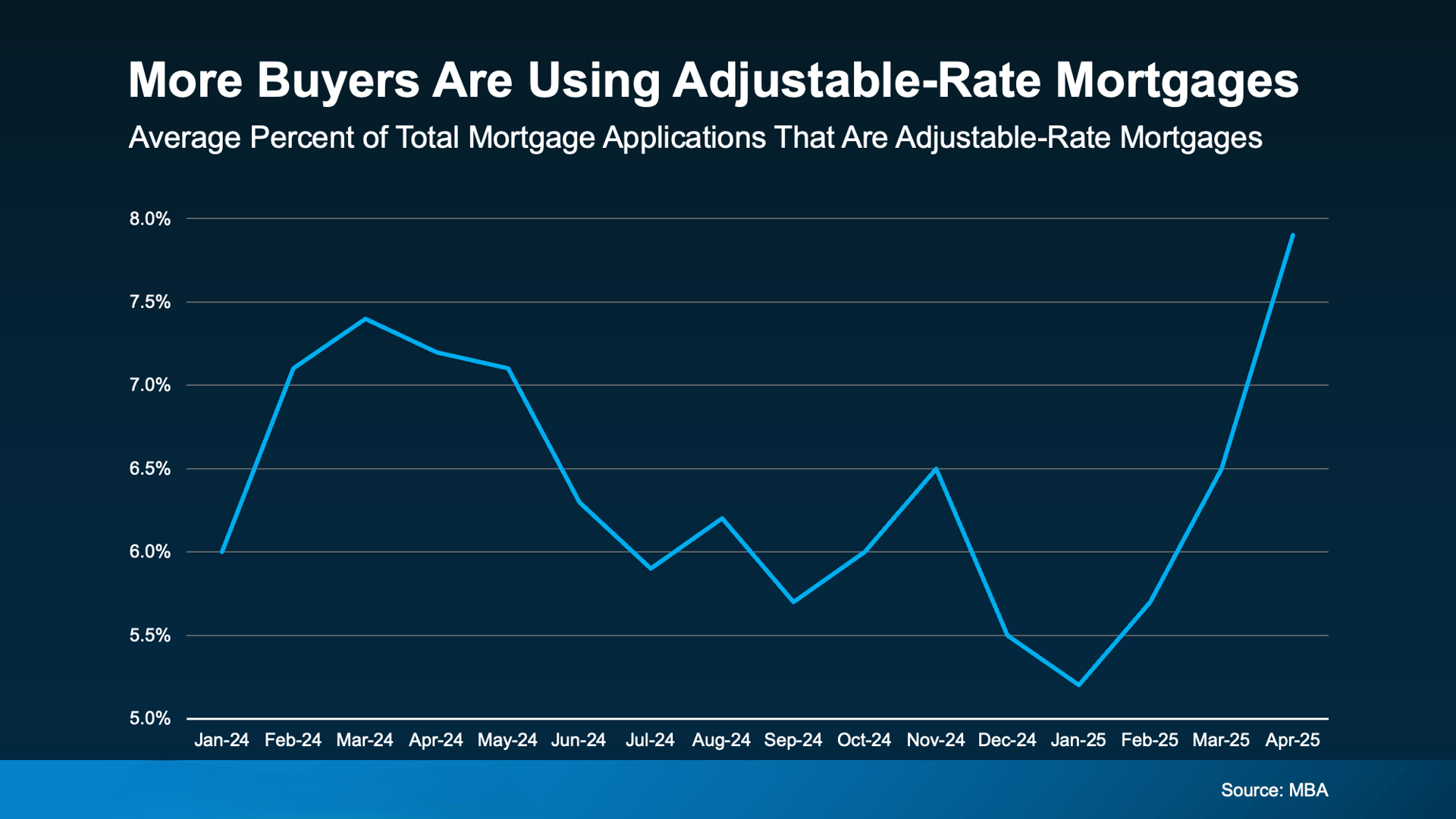

According to the Mortgage Bankers Association, more buyers are giving ARMs another look right now—and it’s easy to see why.

How an ARM Works

With a fixed-rate mortgage, your rate (and monthly payment) stays the same for the life of the loan.

With an adjustable-rate mortgage, you get a lower initial interest rate for a set number of years—often 5, 7, or 10. After that, your rate adjusts based on market conditions. If rates go down, you benefit. If they go up, your payment could rise.

Why Some Buyers Are Choosing ARMs

Here’s the big appeal: a lower initial rate. That can mean a lower monthly payment now—or the ability to afford a little more house.

For some buyers, especially those who plan to move, refinance, or upgrade in a few years, the initial savings can be significant. But ARMs aren’t for everyone. If you’re planning to stay put long-term and rates rise, your payment could eventually increase.

That’s why it’s so important to look at your personal timeline, your financial goals, and your comfort level with risk.

Bottom Line

In today’s market, it makes sense to explore all your options—including ARMs. Just make sure you’re working with a trusted lender who can walk you through the pros and cons based on your specific situation.

And if you’re curious about what mortgage options are available—or how to make the most of your buying power—visit buywithamber.pillarrealestate.com for resources, tips, and tools built just for Central Coast buyers like you.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

[email protected]

1345 Park St. Paso Robles, CA 93446

DRE# 01925434

Amber Johnson | May 29, 2026

Amber Johnson | May 29, 2026

Amber Johnson | May 29, 2026

Amber Johnson | May 29, 2026

Amber Johnson | May 29, 2026

Amber Johnson | May 28, 2026

Amber Johnson | May 28, 2026

Amber Johnson | May 28, 2026

Amber Johnson | May 28, 2026

You’ve got questions and we can’t wait to answer them.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

DRE# 01925434

1345 Park Street

Paso Robles, CA 93446