Buying a Home with Less-Than-Perfect Credit: What to Know

January 12, 2026

January 12, 2026

A lot of would-be homebuyers aren’t sitting on the sidelines because they don’t want to buy. They’re waiting because they think they can’t. And for many, it comes down to one thing: credit.

According to a Bankrate survey, 42% of Americans believe you need excellent credit to qualify for a mortgage. That belief alone is stopping a lot of renters from even starting the conversation. If you’ve looked at your score and assumed homeownership just isn’t realistic yet, you’re not alone.

But here’s the truth most people never hear.

You do not need perfect credit to buy a home.

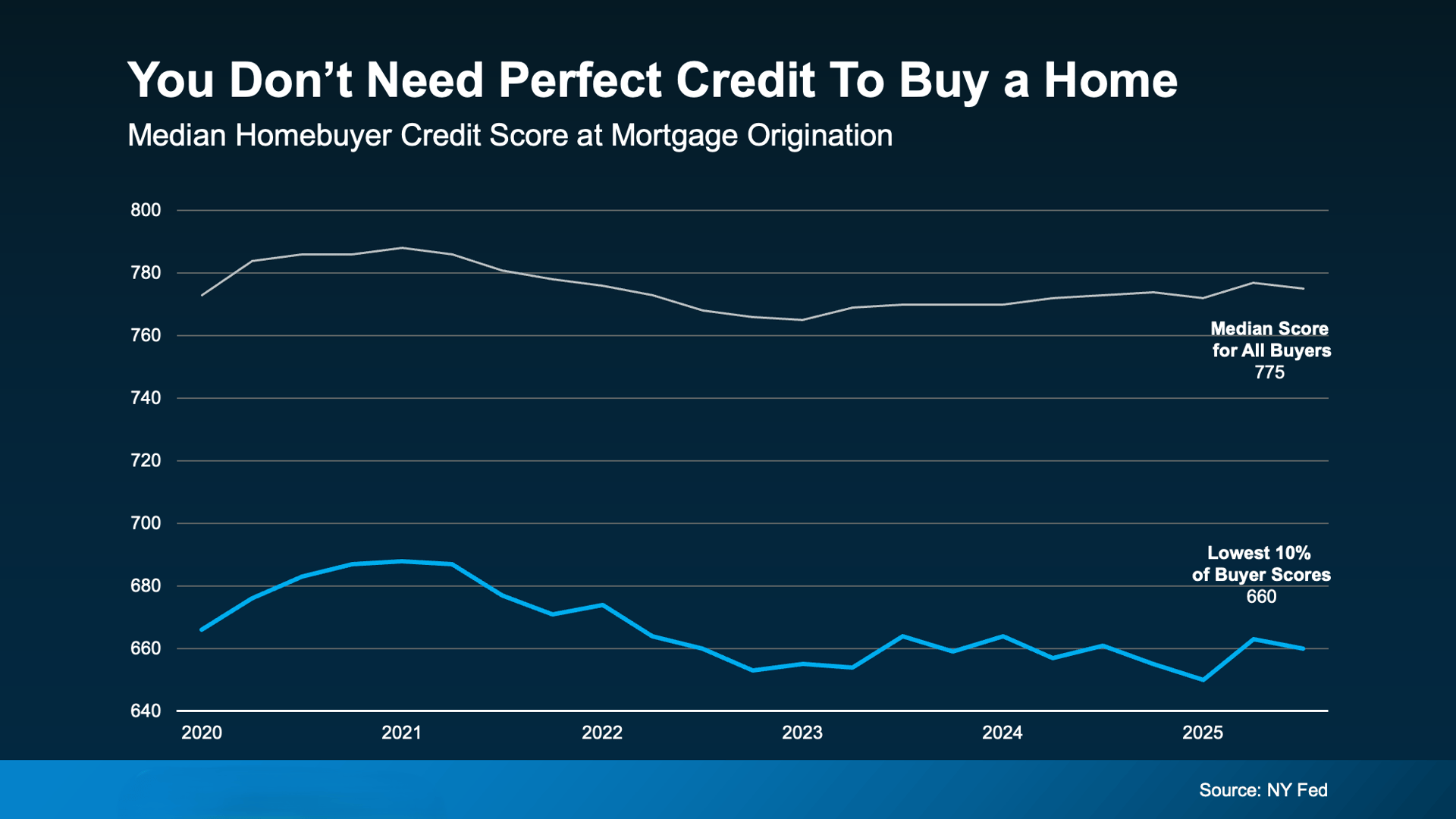

Part of the confusion comes from headlines that focus on today’s “typical” buyer. Data from the New York Fed shows the median credit score for recent homebuyers is 775. That sounds intimidating.

But median doesn’t mean minimum.

When you look closer, real buyers are qualifying with a much wider range of credit scores. In fact, data shows that 10% of recent buyers had scores around 660. Some were higher. Some were lower. But the takeaway is simple: buyers are still getting mortgages well below that 775 number.

And there’s no universal cutoff.

As FICO explains, lenders don’t all play by the same rulebook. Each one sets its own guidelines based on risk tolerance, loan type, and the full financial picture — not just your score.

Translation: your credit score is one factor, not the whole story.

Lenders look at a combination of things, including income, job stability, debt, savings, and payment history. A lower score doesn’t automatically disqualify you, especially if the rest of your finances are solid.

That’s why assuming you “can’t buy” without talking to a lender is often the biggest mistake. Many buyers wait years longer than they need to simply because no one ever showed them their real options.

Your credit score matters — but it doesn’t have to be flawless.

If credit has been the reason you’ve delayed buying, this is your sign to take another look. A quick conversation with a trusted lender can tell you where you actually stand and what steps (if any) make sense next.

You don’t need perfect credit to start the conversation.

You just need accurate information.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

[email protected]

1345 Park St. Paso Robles, CA 93446

DRE# 01925434

Amber Johnson | June 26, 2026

Amber Johnson | June 26, 2026

Amber Johnson | June 26, 2026

Amber Johnson | June 26, 2026

Amber Johnson | June 26, 2026

Amber Johnson | June 26, 2026

Amber Johnson | June 25, 2026

Amber Johnson | June 25, 2026

Amber Johnson | June 25, 2026

You’ve got questions and we can’t wait to answer them.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

DRE# 01925434

1345 Park Street

Paso Robles, CA 93446