Waiting for Rates in the 5s? Read This First

March 9, 2026

March 9, 2026

Mortgage rates have already dipped into the high 5s a couple times this year… and then bounced right back into the low 6s.

If your reaction was, “Great, I missed it,” you’re not alone.

A lot of buyers are treating the 5s like some kind of finish line. Like once rates start with a 5 instead of a 6, everything suddenly becomes affordable.

But when you actually run the numbers, that assumption doesn’t really hold up.

Let’s break it down.

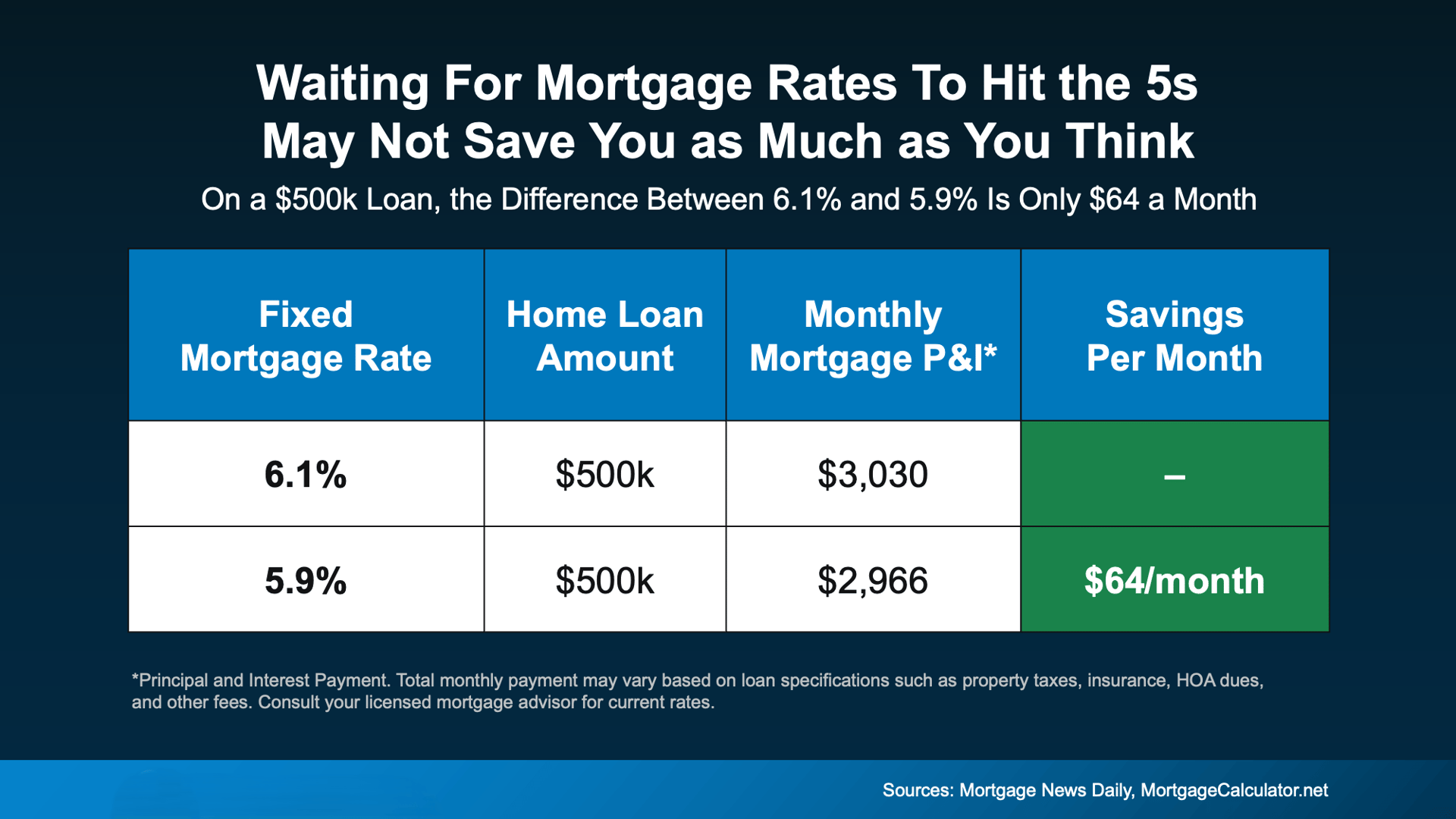

On a $500,000 loan:

That’s a difference of roughly $64 a month.

Not hundreds. Not life-changing.

Just $64.

Yes, over time that adds up. But for most buyers, it’s not the make-or-break number they expect when they say they’re “waiting for the 5s.”

This is where mindset and math don’t always match up.

Seeing a 5 in front of your rate feels like a big win. But financially? It may not move the needle as much as you think.

Here’s the other piece most people miss.

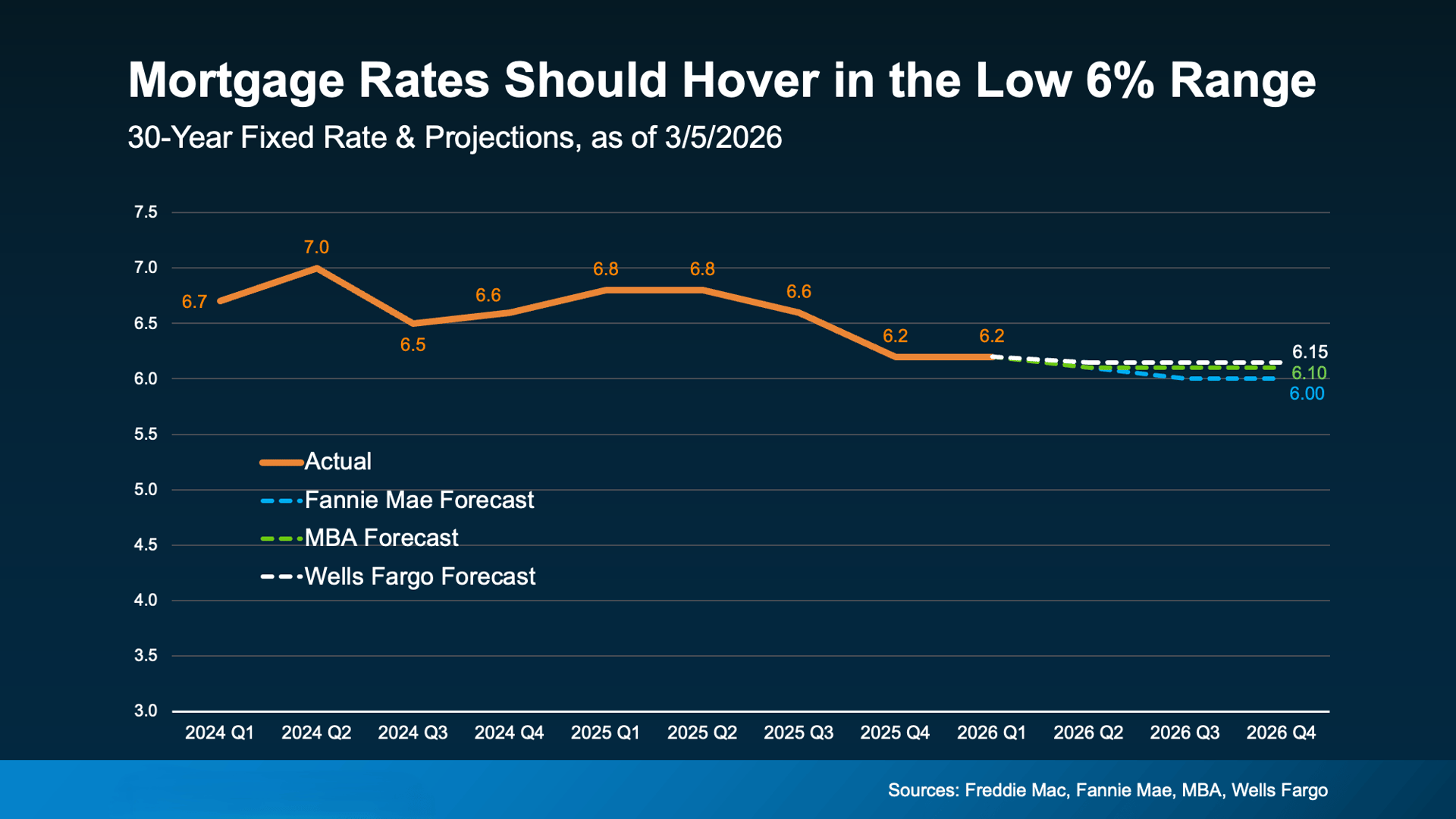

Experts aren’t forecasting a big drop back into the 5s long-term.

Could rates dip there occasionally? Sure.

Stay there? Probably not.

Most projections show mortgage rates hovering in the low 6% range throughout the year.

So if your plan is to wait for a sustained drop well into the 5s, you could be waiting longer than expected… without gaining much financially when it happens.

Instead of asking:

“Did I miss the 5s?”

Ask:

“Does this payment work for me?”

That’s the question that actually matters.

If the payment fits your budget, and the home fits your life, the difference between 6.1% and 5.9% probably isn’t what should hold you back.

And don’t forget rates aren’t permanent.

If they drop later in a meaningful way, you can always refinance.

But you can’t go back and buy the house you passed on.

It’s completely normal to want the best possible rate.

But here’s the reality: the biggest shift has already happened.

Rates were in the 7% range not long ago. Now they’re in the low 6s.

That drop is what’s already improving affordability.

Waiting for another small dip may not deliver the payoff you’re expecting especially if prices rise or competition picks back up at the same time.

Sometimes waiting doesn’t save you money… it just delays your move.

If you’ve been holding out for mortgage rates in the 5s, it may be time to take another look at the numbers.

Because the difference might not be as big as you think and the opportunity you’re waiting for may already be here.

If you want to run the numbers based on your price point and see what’s actually doable, let’s talk. A quick breakdown can give you a lot more clarity than guessing.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

[email protected]

1345 Park St. Paso Robles, CA 93446

DRE# 01925434

Amber Johnson | May 22, 2026

Amber Johnson | May 22, 2026

Amber Johnson | May 22, 2026

Amber Johnson | May 22, 2026

Amber Johnson | May 22, 2026

Amber Johnson | May 21, 2026

Amber Johnson | May 21, 2026

Amber Johnson | May 21, 2026

Amber Johnson | May 21, 2026

You’ve got questions and we can’t wait to answer them.

Amber Johnson, Founder

Pillar Real Estate

805.835.3425

DRE# 01925434

1345 Park Street

Paso Robles, CA 93446